The AI business model war just went live on national television

Super Beef: OpenAI's Ad Gambit Meets Anthropic's Super Bowl Counterpunch

The AI industry's most consequential business model debate stopped being theoretical on Sunday night.

During the Super Bowl, Anthropic aired a series of ads mocking the idea of advertising inside AI assistants — depicting glassy-eyed chatbot personas interrupting users with hilariously bad product placements. The tagline: "Ads are coming to AI. But not to Claude." Ad Age ranked it among the top five spots of the night.

Hours later, OpenAI officially began rolling out ads inside ChatGPT for Free and Go tier users in the US.

The timing wasn't coincidental. The ad launch arrived the same week Altman told employees ChatGPT is "back to exceeding 10% monthly growth," the same week OpenAI is in talks for a $100 billion raise at an $830 billion valuation, and the same week its biggest rival bought a Super Bowl slot to position itself as the anti-ad alternative.

Sam Altman fired back on X, calling Anthropic's ads "clearly dishonest" and framing the debate in access terms: "More Texans use ChatGPT for free than total people use Claude in the US, so we have a differently-shaped problem than they do."

What this means for private market investors: OpenAI is building toward a multi-layered monetization stack — subscriptions, enterprise, API, and now advertising — that starts to look less like a research lab and more like the early architecture of a Google-scale attention business. The ads are priced on impressions, not clicks, and launched without self-serve tools — indicating this is about validating the format, not maximizing near-term revenue. Every free user seeing an ad today is, as Gupta observed, a line item in a future S-1.

For Anthropic, the Super Bowl play was a classic Clay Christensen move: differentiate on what the incumbent can't offer. By publicly committing to an ad-free model, Anthropic is making a strategic bet that trust will be worth more than ad dollars. It's a positioning play aimed squarely at enterprise buyers and premium consumers — the segments that actually drive margin.

Databricks: $7 Billion and a Signal About Staying Private

Databricks completed its expanded financing on Monday — $5 billion in equity plus $2 billion in debt capacity, all at a $134 billion valuation. The round grew from its initial $4B target after JPMorgan expanded its commitment and Microsoft joined late.

The numbers behind the raise tell the real story: annualized revenue of $5.4 billion, up 65% year-over-year. AI products alone now generate $1.4 billion in annualized revenue. Free cash flow positive over the trailing twelve months. More than 20,000 customers including over 60% of the Fortune 500.

CEO Ali Ghodsi told Reuters the $7 billion war chest makes Databricks "really well capitalized, in case there's a winter coming." Translation: they can afford to stay private indefinitely while public software stocks face an AI-driven reckoning. Databricks is now larger than public rival Snowflake ($58B market cap) and trading at a higher implied revenue multiple in the private market than Snowflake commands in public markets.

The IPO is coming — Ghodsi says "when the time is right" — but the ability to raise this kind of capital privately removes any urgency. For secondary market investors, this is the paradox of the current moment: the companies most ready to go public are the ones least compelled to.

Stripe Approaches $140B — and the IPO Question Gets Louder

Stripe is in talks to launch a tender offer that could value the payments giant at $140 billion or more, a jump of over 30% from its $107 billion valuation last fall. Bloomberg and Axios both confirmed the discussions on Sunday.

The trajectory is remarkable: Stripe's valuation hit a low of $50 billion in early 2023, recovered to $65 billion in a 2024 tender, reached $91.5 billion in February 2025, crossed $107 billion last fall, and now appears headed to $140 billion. That's nearly a triple from its trough in under three years.

What's driving the re-rating? Stripe now serves 87% of Fortune 500 companies, 80% of the Forbes Cloud 100, and 78% of the Forbes AI 50. Its Bridge acquisition gave it stablecoin transaction rails. The Metronome acquisition in January strengthened usage-based billing — the pricing model AI companies are gravitating toward.

Goldman Sachs estimates US IPO proceeds could reach $160 billion in 2026. Stripe would be the anchor offering. But every tender offer is also a pressure release valve: by providing liquidity to employees and early investors, Stripe can keep deferring the IPO while maintaining insider morale. The $140B tender is less "pre-IPO pricing" and more proof that the best private companies have built their own parallel public market.

Deal Flow: What Closed Last Week

Harvey AI is reportedly raising $200M at an $11B valuation, led by Sequoia and GIC — barely two months after closing $160M at $8B. The legal AI startup hit $190M ARR by end of 2025, nearly doubling from $100M in August. That's four raises in fourteen months and one of the clearest examples of "velocity pricing" in the current market: when growth accelerates, founders re-price in real time.

Fundamental raised $255M at a $1.2B valuation for its deterministic AI model, Nexus, designed for structured data analysis — a deliberate counter-positioning to transformer-based LLMs.

Resolve AI reached a $1B valuation in a $125M Series A round focused on automated system reliability engineering.

Lunar Energy raised $232M across Series C and D rounds for home battery manufacturing, targeting 20,000 units by year-end and 100,000 by 2028.

Oxide Computer raised $200M led by USIT for its build-your-own-cloud platform, bringing total funding to nearly $390M.

Alphabet sold $20 billion in bonds — its largest-ever US dollar issuance — drawing more than $100 billion in orders. The sale reportedly includes a rare 100-year sterling bond, previously done only by institutions like Oxford University and the Wellcome Trust. Michael Burry noted the historical parallel: Motorola issued a 100-year bond in 1997, the last year it was considered a top-25 US company.

M&A to Watch

Uber is acquiring Getir's delivery operations from Mubadala for $335M and taking a 15% stake in the remaining portfolio for $100M. The consolidation play continues.

Beast Industries — MrBeast's entertainment conglomerate, last valued at $5.2B — acquired Step Mobile, the teen-focused banking app. The creator economy meets fintech in a deal that says more about distribution than financial services.

Advent, FedEx, A&R, and PPF agreed to acquire Polish parcel delivery company InPost for €7.8B. InPost operates 61,000+ automated parcel lockers across Europe — physical infrastructure as a moat in an increasingly digital logistics market.

What We're Reading

Byrne Hobart: The Quiet Rise of the VC SPV

Byrne Hobart flagged a fascinating structural shift in how top-tier VCs manage capital allocation. Benchmark — famously disciplined about keeping fund sizes small — raised two new vehicles specifically to participate in Cerebras's later-stage round. Hobart calls this the "gentleman's pro-rata": the startup doesn't owe the investor follow-on rights, but is happy to let them raise more capital to participate.

The insight for private market observers: the smallest, most selective funds are essentially running two businesses. Their core fund is the brand — the access engine. The SPVs are the profit centers. As Hobart notes, the biggest LPs in these funds aren't just buying returns; they're subsidizing access to follow-on vehicles. The implication is that the "small fund" model isn't actually small — it's a platform with optionality built in.

Tomasz Tunguz: What the Software Selloff Actually Reveals

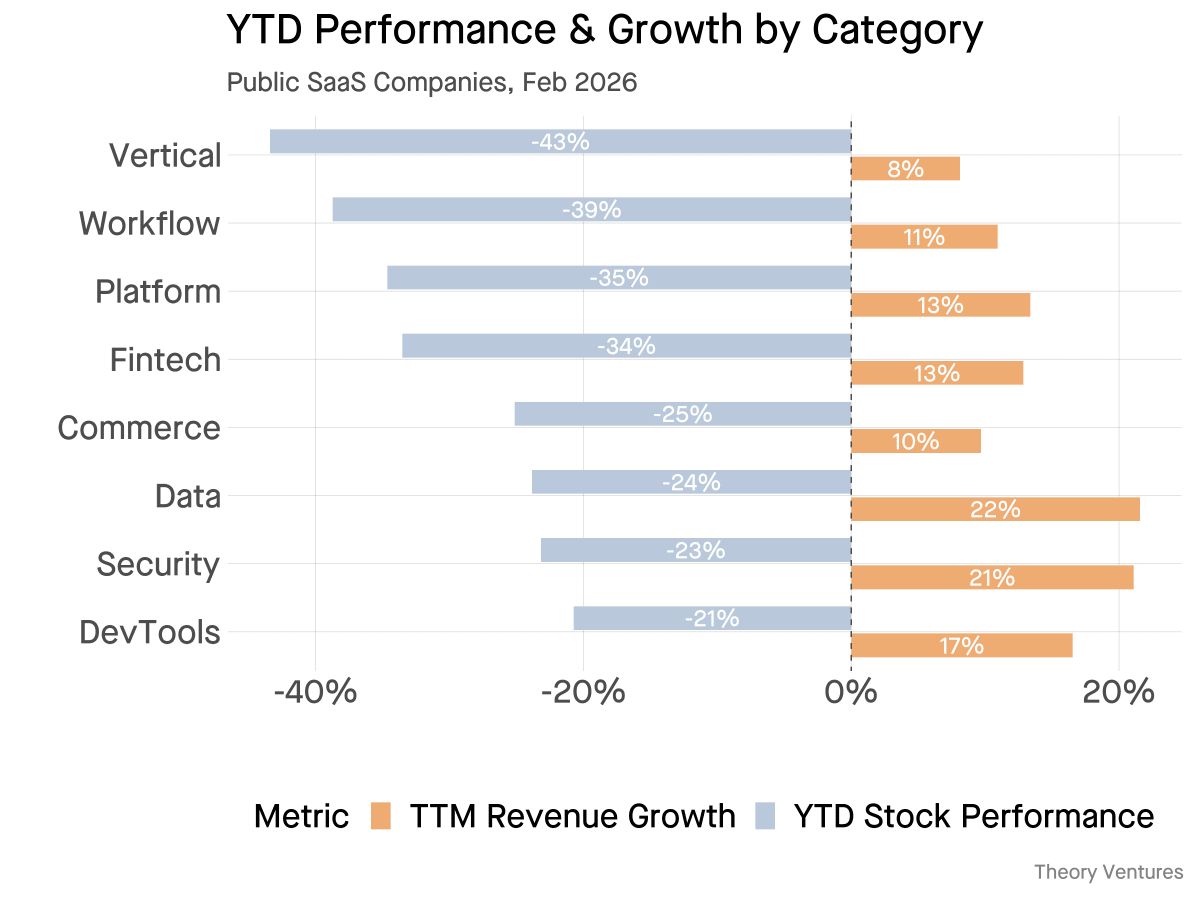

Tomasz Tunguz of Theory Ventures published a sharp analysis of how public markets are pricing AI disruption risk across software categories. The headline: vertical software has fallen 43% this year, while DevTools dropped just 21%. That 22-point gap is the market's implied belief about which categories AI replaces versus which it amplifies.

The counterintuitive finding: vertical software companies like Veeva and Procore — the ones with genuine moats like regulatory barriers and deep integrations — are getting hit hardest. Not because they're most vulnerable to displacement, but because they aren't growing fast enough. The correlation between forward growth rate and forward revenue multiple remains strong at 0.51.

Two clusters emerge: slow growers (vertical software at 8%, workflow tools at 11%) and fast growers (data infrastructure at 22%, security at 21%). The gap between these clusters in year-to-date performance is roughly 20 percentage points.

Tunguz's core question is the one every enterprise software investor should be asking: can a company grow when AI makes its customers more efficient rather than more numerous? Atlassian's recent earnings — 5 million Atlassian Intelligence MAUs, cloud revenue crossing $1B for the first time, RPO up 44% — suggest the answer for developer tools is yes. For workflow software, investors are less certain.

📊 Data Point of the Day

65%

Databricks' year-over-year revenue growth rate in Q4, accelerating from 55% the prior quarter. The company that sells picks and shovels for the AI gold rush is itself growing faster than most of the AI companies it serves.

🎓 Manual

Gentleman's Pro-Rata

A gentleman's pro-rata is an informal arrangement where a startup allows an existing investor to participate in a new funding round even though that investor doesn't have contractual pro-rata rights. Unlike a standard pro-rata clause — which legally entitles an investor who owns, say, 5% of a company to invest enough to maintain that 5% in subsequent rounds — a gentleman's pro-rata is granted at the company's discretion. It's a signal of strong relationships and mutual confidence.

As Byrne Hobart noted this week, this mechanism is particularly relevant for small, concentrated funds like Benchmark that intentionally limit their initial check sizes but want the option to double down on winners.

What We're Watching

- OpenAI's ad conversion data. Ben Bajarin argues AI queries will enable much higher relevance targeting and conversion. If that thesis proves out, the ad revenue line in OpenAI's financials could scale faster than anyone expects — and the pressure on Anthropic's ad-free model intensifies.

- The warning shot. Stock plunged 20%+ after weak Q1 guidance, as management flagged "rising pressure from agentic AI tools." This is the first major public-company earnings call to cite AI agents as a direct competitive threat to workflow software. It won't be the last.

- Fintech VC momentum. PitchBook reports fintech deal value hit $17.3B in Q4, pushing full-year funding to $42.8B — the highest since 2022. Median deal sizes and valuations hit records. The sector is experiencing a genuine recovery, not just a few mega-rounds pulling up the average.

Paul leads editorial at Augment, building Pulse into the private markets' go-to intelligence source. He also develops editorial content strategies for startups and venture capital firms. Previously, he spent 15 years as a business and opinion journalist at The New York Times, Fortune, Fast Company, Reuters, and more. He believes transparency creates liquidity—and that someone should actually publish what private shares are trading for. He lives in Marin with his wife and two rescue dogs, and wishes he had more time to surf.

Learn more

FOR ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. Registration with the SEC does not imply a certain level of skill or training. Neither Augment Advisors, LLC nor Augment Capital, LLC provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.