The Day the Buy Button Disappeared

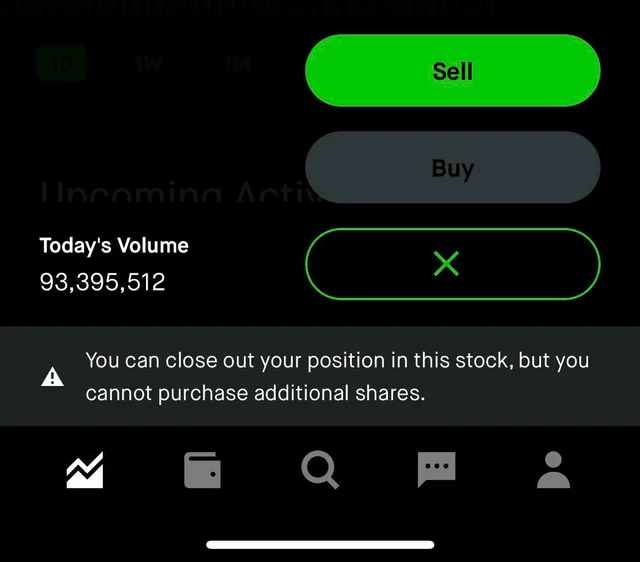

January 28, 2021. In a Reddit-fueled trading frenzy powered by equal parts technical analysis, childhood nostalgia, and memeification, GameStop hits $483 per share, up from $2.50 barely eight months prior. Then Robinhood pulls the buy button.

Retail traders watch their positions crater in real time, unable to add to them, while institutional investors could still trade freely. The rage was immediate: death threats to Robinhood employees, congressional hearings within weeks, a viral hashtag accusing the company of market manipulation, and eventually a $30 million settlement with Massachusetts regulators who accused the platform of gamifying trading and failing to protect inexperienced investors.

Five years later, the person at the center of that chaos is still thinking about it.

"What happens when you combine slow, outdated financial infrastructure with unprecedented trading volume and volatility?" wrote Vlad Tenev, Robinhood's CEO, in a post marking the anniversary. His answer: "Massive deposit requirements, trading restrictions, and millions of unhappy customers."

Tenev's retrospective is notable for what it reveals about the actual cause: The trading halt wasn't a conspiracy—it was a $3.7 billion clearinghouse margin call. The then two-day order settlement cycle required brokerages to post enormous collateral during volatility spikes. Robinhood simply didn't have the cash to do it. Within 72 hours, they raised $3.4 billion in emergency funds to stay solvent, but the damage had been done.

Market regulators have since shortened the standard settlement cycle to T+1. But Tenev argues that's not enough: "In a world of 24-hour news cycles and real-time market reactions, T+1 is still far too long, particularly when you factor in that it really means T+3 on Fridays, or T+4 on long weekends."

His post proposes a solution: tokenized equities with real-time blockchain settlement. Five years ago, that would have sounded like crypto wishcasting. Now it's infrastructure reality. The NYSE announced this month it's developing a platform for 24/7 trading of tokenized securities with instant settlement. Nasdaq filed a proposed rule with the SEC in September that would enable tokenized equity settlement by Q3 2026. DTCC plans to pilot its tokenization service in the first half of this year.

The infrastructure that broke in January 2021 is being rebuilt. But the more interesting question is what happened to the investors who lived through it.

What Retail Learned

The narrative that emerged from GameStop was "retail vs. Wall Street"—a David-and-Goliath story about coordinated buying overwhelming hedge fund short positions. Five years later, that framing missed what actually mattered.

What GME revealed wasn't that retail investors wanted to beat hedge funds. It was that a meaningful segment of individual investors would accept illiquidity, information asymmetry, and counterparty risk if they believed the asymmetric upside justified the friction. They didn't flee when the rules changed mid-game. Many bought more.

That psychology didn't disappear when GME collapsed. It migrated.

Individual investor participation in U.S. equities has risen to nearly 20% of daily trading volume, up from low single digits before Covid, according to Jeff Shen, co-chief investment officer at BlackRock. On high-volume days, retail can hit 40%, per Robinhood's chief brokerage officer.

"People had assumed that once Covid cleared up, and everybody went back to their daily lives, that this retail participation would recede and go back down," Steve Quirk of Robinhood told CNBC this week. "What surprised me a little bit is how strongly it's continued."

But the investors who emerged from GME didn't all retreat to index funds. Some went looking for asymmetry in markets where friction was structural—where limited access meant limited competition.

The Private Markets Parallel

Consider what GME buyers accepted in January 2021:

- Illiquidity: Couldn't exit when they wanted to

- Information asymmetry: Retail had less data than institutions

- Extreme volatility: 50%+ swings in single sessions

- Counterparty risk: Brokers changed the rules mid-trade

Now consider what private market investors accept:

- Illiquidity: Transactions can take one day weeks depending on deal structure

- Information asymmetry: No public filings, limited price discovery

- Valuation uncertainty: Last funding round ≠ current market price

- Transfer friction: ROFR, company approval requirements, accreditation gates

The friction profiles rhyme. The difference is what's on the other side of the trade.

GME buyers were betting on a short squeeze—a one-time technical dislocation. When the squeeze ended, so did the thesis. Private market investors are buying stakes in operating businesses with revenue, customers, and identifiable paths to liquidity. The friction isn't a bug to be exploited; it's a gate that filters out less committed capital.

This isn't to say private markets are "better" than public markets—that framing would be wrong. Private markets have real friction that can work against investors: companies block transfers, ROFR provisions kill deals, and price discovery remains opaque. But for investors with the risk tolerance, time horizon, and accreditation to participate, the tradeoffs are at least legible. You know what you're signing up for.

GME investors found out mid-trade that the rules could change.

The Numbers

Secondary market volume hit $226 billion in 2025—the first time above $200 billion and a 41% increase from 2024, according to Evercore. That's nearly 4x the volume from five years ago, when GameStop dominated financial media.

About a third of the capital deployed in secondary PE markets in 2024 came from individual investors, per BlackRock. Lazard expects retail capital to be a key driver of secondary market growth this year, noting that inflows from individuals continue to accelerate.

Bain estimates that capital from sovereign wealth funds and individual investors will account for 60% of future private markets AUM growth through 2033.

The investor psychology that powered the GME trade—willingness to accept friction for asymmetric opportunity—didn't disappear. It found a different market.

📊 Number of the Day

20%

Individual investor share of daily U.S. equity trading volume—up from low single digits before the pandemic. Five years after GameStop, retail is no longer a sideshow.

📖 Manual

T+1 Settlement

The standard settlement cycle for most U.S. securities transactions: trades settle one business day after execution. The SEC shortened settlement from T+2 to T+1 in May 2024 to reduce counterparty risk. As Tenev noted in his anniversary post, T+1 still creates delays on weekends and holidays—which is why exchanges are now pursuing blockchain-based instant settlement.

Feeling nostalgic? There are a number of GameStop documentaries out there that paint the players in various lights of villainy and flattery. Gaming Wall Street from HBO Max is considered among the more technical looks, so naturally it’s the trailer we’ll put here:

Fundings

Decagon triples valuation to $4.5B with $250M Series D — The AI customer service platform raised from Coatue and Index Ventures yesterday, six months after reaching unicorn status. Customers include Chime, Hertz, and Oura.

Vention raises $110M to scale industrial automation — The Canadian robotics company landed a Series D led by Investissement Québec with participation from Nvidia's NVentures. Over 25,000 robots deployed across 4,000 factories.

Paul leads editorial at Augment, building Pulse into the private markets' go-to intelligence source. He also develops editorial content strategies for startups and venture capital firms. Previously, he spent 15 years as a business and opinion journalist at The New York Times, Fortune, Fast Company, Reuters, and more. He believes transparency creates liquidity—and that someone should actually publish what private shares are trading for. He lives in Marin with his wife and two rescue dogs, and wishes he had more time to surf.

Learn more

FOR ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. Registration with the SEC does not imply a certain level of skill or training. Neither Augment Advisors, LLC nor Augment Capital, LLC provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.