When a company you invested in through a special purpose vehicle (SPV) goes public, the transition from private to public ownership can raise important questions. Unlike direct stock ownership, SPV investments add layers of structure, discretion, and timing that shape how and when limited partners (LPs) realize returns.

This blog walks through what happens when an SPV-backed company performs an initial public offering (IPO), outlining the mechanics of distributions, lockup periods, fees, manager discretion, and broader implications for private secondary markets.

Understanding SPVs in the pre-IPO context

An SPV is a legal entity formed to pool investor capital into a single company, typically a late-stage startup. SPVs have become a mainstay of private market investing because they provide access to otherwise closed opportunities and create efficiency in managing groups of investors.

In practice, an SPV acts like a “micro-fund” for one investment. Investors own membership interests in the SPV, which in turn owns shares of the company. When that company IPOs, the SPV must determine how to convert its holdings into value for its LPs.

Cash vs. in-kind distributions

The first question most LPs ask is whether they will receive cash proceeds or actual shares of the newly public company. The answer depends on the SPV’s governing documents and the manager’s strategy.

- Cash Distributions: Many SPV managers sell shares at or shortly after the IPO and distribute cash. This provides immediate liquidity and simplifies administration, though it locks in gains (or losses) at the moment of sale.

- In-Kind Distributions: Alternatively, some managers transfer public shares directly to LPs, making each investor a shareholder. This lets LPs decide whether to hold or sell, but requires them to manage brokerage accounts, cost basis, and taxes on their own.

Some managers may offer LPs a choice, while others set this in advance in the SPV agreement. LP preference often depends on investment goals: some value liquidity, while others want long-term exposure to potential compounding growth.

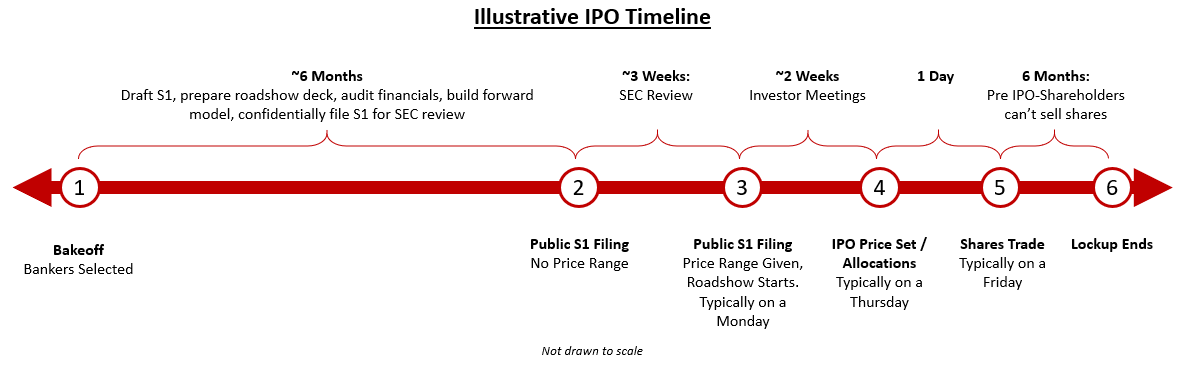

Lockup periods and timing

IPO lockups, typically 180 days, restrict insiders and early investors from selling immediately. For SPVs, this means distributions usually cannot occur until the lockup expires.

- Cash Distributions: Not possible until the SPV can sell its shares after the lockup.

- In-Kind Shares: Sometimes distributed before lockup expiration, but subject to resale restrictions.

Some lockups are staggered, releasing shares in tranches. Others may extend if the company’s price drops below a threshold. Understanding these restrictions is critical, since market volatility during a lockup can significantly impact realized returns.

Fees and expenses at IPO

SPV fees do not end at IPO. In fact, they can increase.

- Management Fees: If applicable, they may continue until the SPV is fully wound down.

- Carried Interest: Carried interest applies to realized gains, including those recognized at IPO.

- Transaction Costs: Legal updates, fund administration, transfer agent fees, and brokerage costs may all reduce LP proceeds.

LPs receiving in-kind shares should also plan for brokerage fees, reporting costs, and tax preparation tied to their holdings.

Manager discretion and hold-back rights

Most SPV agreements grant managers wide discretion over when and how to distribute proceeds. While this discretion exists to protect LP value, it can delay distributions even after the lockup period.

Managers may hold back distributions to:

- Avoid unfavorable market conditions.

- Wait for staggered lockup releases.

- Consolidate distributions into a single tranche.

Still, fiduciary duty requires managers to act in the LPs’ best interest. Excessive or unjustified delays can raise concerns, underscoring the importance of understanding your SPV’s terms before investing.

Voting, information, and control rights

As an SPV investor, you do not directly hold shares in the operating company. Instead, the SPV manager controls voting rights, information flow, and corporate communications.

This means:

- LPs do not receive proxy statements, annual reports, or direct shareholder materials.

- The manager decides how to vote on company matters prior to an IPO.

- Only once in-kind shares are distributed do LPs gain direct shareholder rights.

This structure underscores the importance of trusting the manager’s judgment and transparency.

Tax considerations

SPVs are typically pass-through entities, so gains flow to LPs, reported via Schedule K-1. Tax outcomes may depend on distribution type:

- Cash Distributions: Capital gains (short- or long-term depending on holding period) recognized upon sale by the SPV.

- In-Kind Shares: LPs inherit the SPV’s cost basis and holding period. The distribution itself may or may not be taxable depending on structure.

Large IPO gains concentrated in a single tax year can potentially push investors into higher brackets or trigger the Net Investment Income Tax. Professional tax advice is strongly recommended.

Implications for the secondary market

The way SPV IPOs play out has ripple effects in private secondary markets:

- Liquidity Timing: Because of lockups and manager discretion, IPOs do not always mean instant liquidity for LPs. Secondary platforms offering pre-IPO access like Augment can help investors exit earlier, often before IPO lockups even begin.

- Valuation Volatility: IPO pricing can inflate private valuations, but post-lockup declines can erode returns. Sophisticated investors may prefer secondary exits ahead of IPO risk.

- Pricing Benchmarks: IPO outcomes can serve as important benchmarks for private market pricing. SPVs tied to companies approaching an IPO often see heightened secondary activity as investors position ahead of a public listing. This creates a feedback loop where private secondary pricing can become an early indicator of public market appetite.

- Expanding Access: SPVs give investors fractional exposure to late-stage companies, something that was historically limited to large venture funds. By bringing more investors into high-growth names pre-IPO, SPVs expand access and help deepen overall liquidity in the private secondary ecosystem.

Key takeaways for investors

- Know your SPV documents: Distribution method, fee structure, and manager discretion all hinge on the operating agreement.

- Plan for lockups: IPO does not mean immediate liquidity. Returns may be delayed six months or longer.

- Budget for fees and taxes: Both can materially affect net proceeds.

- Trust the manager: Since you lack direct shareholder rights, transparency and alignment are critical.

Conclusion

An IPO is a milestone for any startup, but for SPV investors it is only part of the journey. Cash versus in-kind distributions, lockup timing, fees, and manager discretion all determine how and when LPs actually realize value.

As private markets continue to grow and platforms introduce more efficient secondary trading options, SPVs are evolving from one-off vehicles into building blocks of a more liquid, accessible private market. For investors, understanding how IPOs affect SPVs is essential to navigating this transition and making informed decisions about pre-IPO exposure.

*Securities transactions are executed on Augment Capital, LLC's ATS and offered through Augment Capital, LLC (member FINRA/SIPC).

Important Disclosures: Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. Additionally, past performance of private securities does not indicate or predict future results.

Jack is a serial entrepreneur and investor at Augment, where he works alongside the CEO on strategy and operations. He brings over three years of experience in private secondary research, following a career in venture capital evaluating early- and growth-stage companies. Having worked at five different startups, he remains an active investor in the ecosystem. He believes the best private companies should not be reserved for the 1%—and that transparency and regulation are the only ways to truly democratize the private markets. He is currently based in Austin, and claims that he will one day move to Japan (or so he says).

Learn moreRelated posts

View more

FOR ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. Registration with the SEC does not imply a certain level of skill or training. Neither Augment Advisors, LLC nor Augment Capital, LLC provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.