Read Pulse

Working for a startup can be both an exciting and overwhelming career move. Startups carry several perks. One of the biggest is a compensation package complete with stock options — a confusing, but potentially very lucrative opportunity.

Many employees don’t know the difference between ISOs and NSOs — the main types of startup stock options — or how those differences could affect their finances. Below, we’ll break down the two options and their pros and cons, plus what to keep in mind when making decisions.

Stock options, sometimes referred to as equity options, give an employee the right to purchase stock in their company at a set price, often called a “strike price.” They allow employees to have ownership in their company, directly tying its success to their financial futures.

Ideally, an employee purchases shares at a certain price and is able to sell them later for much more, after the company has evolved and matured.

Proponents say stock options boost employees’ morale and incentivize them to work harder. Most stock options come with a vesting period that stretches over a couple of years, encouraging employees to remain with the company for longer. If they leave before the period is over, they might not receive their full award.

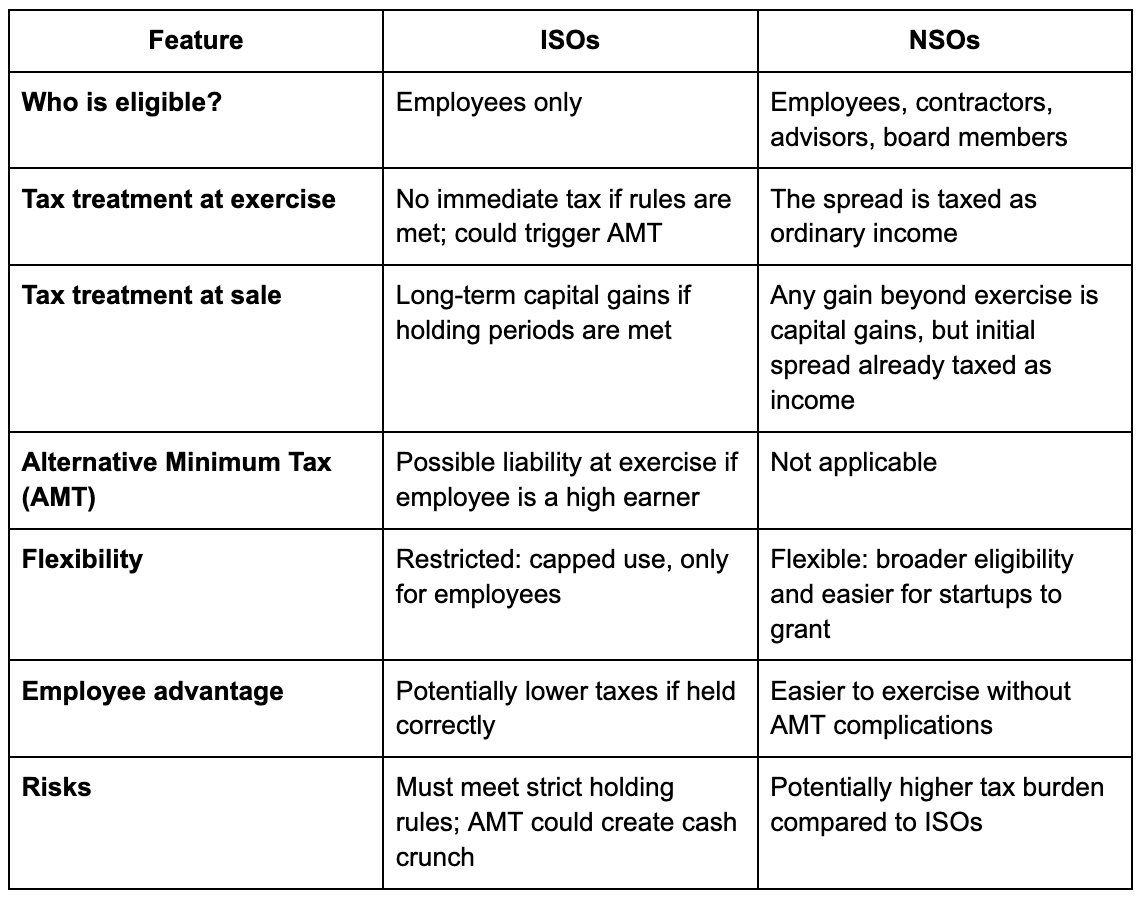

The key differences between these two types of stock options come down to taxes and who can qualify.

ISOs are tax-advantaged stock options reserved solely for employees. This means other people associated with the company, such as advisors, contractors, or board members, are not eligible.

ISOs offer better tax treatment, as long as the employee meets the holding period rules. For an ISO sale to qualify, it must be made at least two years after the grant date and one year after the options were exercised, or purchased. If the employee makes a qualifying sale, they’ll report only the capital gain. If the sale doesn’t meet the holding period requirements, the employee will have to report any difference between the share price and exercise price as earned income.

To take advantage of this option, employees generally must hold on to their stock for a longer time period. And some high earners who cash in on ISOs might be at risk of owing the alternative minimum tax (AMT). Strategic tax planning around startup equity — including AMT and QSBS — can help you reduce exposure and keep more of what you earn.

NSOs offer a more flexible stock option for a broader group of people: employees, advisors, or board members are all eligible. The stockholder will pay ordinary income tax on the “spread,” or the difference between the market and strike prices, whenever they exercise their shares.

Unlike with ISOs, anyone exercising an NSO won’t have to worry about the AMT. But paying income tax on the spread can be less favorable than having to report only capital gains, and might result in a higher tax burden.

Startups will often include stock options as part of their compensation packages. Before signing a deal that includes ISOs or NSOs, prospective employees should assess the company’s potential for growth — and, in turn, the potential for their shares to appreciate in value. That includes taking a closer look at the company’s 409A valuation, which directly influences your strike price and tax treatment.

The rule of thumb for when to sell your shares is relatively straightforward: whenever their value is higher than what you purchased them for. And even if your startup hasn’t gone public by the time you want to sell, platforms like Augment* can help match you with a buyer.

Employees should also keep in mind the potential tax consequences that come with each option. The best way to anticipate these implications is to work with a tax professional.

ISOs aren’t “better” than NSOs, and vice versa. The best path for you will depend first and foremost on what options your startup offers, and then on your risk tolerance and the stage of your company. Structuring your equity with liquidity in mind can also help ensure you're set up for stronger outcomes—especially if your situation changes before a traditional exit.

*Securities transactions are executed on Augment Capital, LLC's ATS and offered through Augment Capital, LLC (member FINRA/SIPC).

Important Disclosures: Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. Additionally, past performance of private securities does not indicate or predict future results.

FOR ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. Registration with the SEC does not imply a certain level of skill or training. Neither Augment Advisors, LLC nor Augment Capital, LLC provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.