Read Pulse

If you have equity in a startup, you could be eligible for serious tax breaks when you sell. Depending on when the stock was issued, you may be able to exempt as much as $150 million or 10 times the original basis of the stock in capital gains.

Whether you're a founder, employee, or early-stage investor, understanding the tax benefits of startup equity could save you millions of dollars.

Wondering what the catch is? There's no catch, per se. But it’s important to make sure you and your company meet the requirements and make a plan so you can maximize your exemptions. Outside of that, think of it as a reward for the stress, hard work, and risk that's involved in getting a small business off the ground.

President Trump's One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, expanded the QSBS criteria. We've included the updated figures in this article, as well as a summary of how QSBS works for stock issued before and after the Act was signed.

Read on for everything you need to know about qualified small business stock.

Qualified Small Business Stock (QSBS) is a type of stock issued by startups and early-stage companies. It plays a powerful role in early-stage private investing strategies, especially for founders and investors looking to unlock long-term value. It QSBS falls under IRS Section 1202, an incentive designed to encourage entrepreneurship. To qualify, the company needs to be a C-Corp with less than $50 million in assets at the time the shares are issued ($75 million if issued after OBBBA). LLCs and S-Corps don't qualify.

There are some other important criteria too. You need to be an individual taxpayer, not a corporation. You need to hold the stock for more than five years (three if the stock was issued after 4 July 2025). The stock needs to come directly from the company, whether that's through stock options, founder grants, or participating in a funding round. Stock purchased on secondary markets does not qualify. (Though, as we'll see shortly, pre-ipo investment platforms could help you sell your QSBS.)

Finally, only certain industries can be qualified as small businesses. Most tech, manufacturing, and retail businesses are eligible, as long as the company uses 80% of its assets in that activity. AI-driven sectors, for example, are often structured to meet QSBS eligibility and are drawing strong interest from early investors. Unfortunately, service-based industries, such as health, accounting, law, and financial services, won't qualify. Neither will hotels and farming businesses.

If you want to get the full tax benefits from the QSBS exemption rule, it is important to fully understand the nuances of what is quite an unusual tax benefit. You'll need to collect various bits of paperwork, including the company's incorporation documents and financial statements, to show it met the requirements when the stock was issued.

The basics: If the stock was issued after September 2010, and you and the company fit the criteria above, the rule allows you to exempt 100% of eligible gains of up to $10 million or 10x your original investment — whichever is greater.

If the stock was issued after the signing of the OBBBA on 4 July 2025, you can exclude eligible gains of up to $15 million or 10x your original investment.

The specifics: If you're ready to sell your qualified stock, the following details may help you maximize your exemptions. A tax adviser can help you make a plan and ensure you meet all the requirements.

Let's say you have stock that's now worth $25 million in a qualified business. The stock was issued before July 2025, had $1.5 million of basis, and you've held it for five years. You might sell $15 million of stock in this tax year using the 10x exemption, and another $10 million next year. That way you'd be able to exclude the whole amount from capital gains tax. If we assume a 20% federal capital gains tax, that could translate to $5 million in tax savings.

With millions of dollars in potential tax savings on the table, it's worth jumping through some hoops to ensure you and your company qualify.

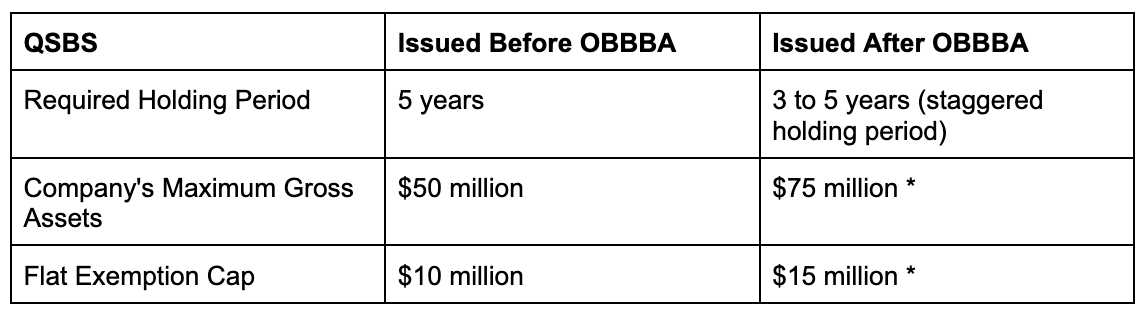

The OBBBA expanded the QSBS criteria in three important ways. For QSBS issued after the OBBBA was signed:

To summarize, here's how the OBBBA will expand QSBS benefits:

* To be adjusted annually for inflation

Private secondary markets give founders, employees, and early-stage investors more flexibility in how (and when) they realize gains. Timing your exit in the private markets is especially useful when planning around things like QSBS holding periods. You no longer have to wait for an IPO or acquisition to cash out—companies like Augment Capital* can connect you with qualified investors who are looking for high-growth opportunities with top pre-IPO companies.

That may mean you can sell QSBS on a private stock marketplace at a time that's right for you. Perhaps that's the point when the three- or five-year holding period is up. Or the year that best suits your tax strategy to maximize exemptions. There can be a lot of moving parts when ensuring that both you and the company meet the criteria, but once you're ready, Augment makes the selling as easy as possible.

*Securities transactions are executed on Augment Capital, LLC's ATS and offered through Augment Capital, LLC (member FINRA/SIPC).

Important Disclosures: Investing in private securities involves substantial risk, including the potential loss of principal. Private securities are typically illiquid, have limited pricing transparency, and often require longer holding periods. These investments are available exclusively to qualified accredited investors and offer no guarantee of returns. Additionally, past performance of private securities does not indicate or predict future results.

This information is for general guidance only and does not constitute tax or investment advice. Consult a qualified professional before making investment decisions.

FOR ACCREDITED INVESTORS ONLY: Under federal securities laws, private market investments on this platform are available exclusively to Accredited Investors. Verification of status required before investing. Private investments involve significant risks including illiquidity, potential loss of principal, and limited disclosure requirements. "Augment" refers to Augment Markets, Inc. and its affiliates. Augment Markets, Inc. is a technology company offering software and data services. Investment advisory services are offered through Augment Advisors, LLC, an SEC-registered investment adviser. Brokerage services are offered through Augment Capital, LLC, an affiliated broker-dealer and member FINRA/SIPC. Registration with the SEC does not imply a certain level of skill or training. Neither Augment Advisors, LLC nor Augment Capital, LLC provide legal or tax advice; consult your attorney or tax professional regarding your specific situation. For additional information, please refer to Augment Advisors, LLC’s Form ADV Part 2A (Firm Brochure) and FINRA BrokerCheck.